Happy Veteran’s Day. Please click on the link to see a 30 second video of my Dad during WWII. He’s the handsome guy on the left. The sailor on the right is his good friend, Larry Netka.

Create your own video slideshow at animoto.com.

Happy Veteran’s Day. Please click on the link to see a 30 second video of my Dad during WWII. He’s the handsome guy on the left. The sailor on the right is his good friend, Larry Netka.

Create your own video slideshow at animoto.com.

Many people need a copy of their federal income tax return in order to get a mortgage or file for financial aid. You can order a copy of your return from the IRS for $57, but most people can get everything they need with a tax return transcript.

Many people need a copy of their federal income tax return in order to get a mortgage or file for financial aid. You can order a copy of your return from the IRS for $57, but most people can get everything they need with a tax return transcript.

I was just looking at another website that offered to get your transcript for you, for a fee of $99. But you can get that transcript directly from the IRS for free and it’s easy to do. Here’s how:

Call the IRS main phone number: 1 (800) 829-1040

You’re going to hear a computerized woman’s voice asking you questions. You will select “2” for information on your personal taxes.

Next, you will select “1” for information about your tax history.

Next you’ll enter “2” to get a transcript.

[Just so you know, you can call the IRS at 1 800 829-1040, type in 2, then 1, then 2 and it will take you to this next part. You don’t have to listen to the whole computerized menu offerings.]

After that, you’ll be asked for your social security number. If you’re married, use the social security number of the spouse listed first on the return. They’ll be questions to verify your address. They’ll ask what year you need the transcript for, but it’s all computer automated and you respond with your telephone keypad. You can order up to 10 transcripts if you need them.

See how easy that is? It will take 5 to 10 days for your transcripts to arrive at your address. And you won’t have wasted any money!

If you must have a photo copy of your tax return, you’ll need to file form 4506. It will cost you $57 and can take up to 60 days to receive. Before you spend the money, be sure to check with the bank and see if a transcript won’t be acceptable. Here’s a link to the form if you need it. Form 4506

I’ve done a lot of posts about unusual small business deductions, but I haven’t done anything about the basics. If you’re new to the small business world, that’s what you really need to know. These are some of the basic, core facts that you need to know to prepare your small business taxes.

First, if you’re just starting out, and you haven’t filed any papers like articles of incorporation, and you don’t have any partners, then you’re considered to be a sole proprietor. Your business tax return goes on a form called a Schedule C, and that’s part of your regular 1040 form. Don’t file your personal taxes and then try to file your business return later, they’re one and the same thing.

What if I’m an LLC? An LLC is a limited liability company, it’s not a corporation. Most LLC’s will file as sole proprietors unless they have filed documents to be taxed as an S or C corporation. (Then they file corporated tax form 1120S or 1120.) LLCs that have partners will file partnership returns, form 1065. This post is about sole proprietors who file Schedule C with their 1040 return.

A popular question I hear is, “How much money do I have to make to file a return?” According to the IRS, if you make over $400 of self employment income, you are required to file a federal tax return. This is very different from the minimum filing requirements of regular returns. Once you’ve made over $400, that income is subject to self employment tax and the IRS is very keen on collecting your self employment tax.

Another common question is, “How will the IRS know that I’ve made over $400?” The easiest way for the IRS to find out your income, assuming that you haven’t reported it yourself, is from forms 1099MISC. Many companies hire people as contract labor and don’t withhold payroll taxes. If you make over $600 from them, they are required by law to give you a form 1099MISC, showing how much they paid you. A copy of that form also goes to the IRS. That’s the most common way small businesses can get in trouble for underreporting their income.

Another way the IRS can find out that you’re not reporting your income is through your bank records. Let’s say for example that all of your business transactions are for cash and you never receive a 1099MISC. Although you wouldn’t get caught as quickly, let’s say you had an annual income of $20,000 from your all cash business. Your spending would be out of line with your income and could trigger an audit. A quick look at your bank statements would prove you weren’t reporting your income. If you’re serious about starting a real business, do it right and have a plan for handling your taxes. It will save you a lot of trouble in the future.

Small business income, unlike wage income, has one big disadvantage–it get’s taxed twice. First, it’s taxed at your normal tax rate and then again at the self employment tax rate (15.3%.) Let’s say you’re already in the 25% tax bracket for another job you have, your self employment income would then be taxed at 40% (the 25% plus the 15%.)

Small business income also has one big advantage–you can reduce your self employment income by any expenses you had acquiring that income. You may even have more business expenses than you have income, in that case, you can use your business losses to reduce your regular income, that lowers your overall income tax bill. Now you don’t want your business to be losing money every year (that’s not really good business practice.) But when you’re starting up, being able to deduct your losses is very helpful.

So what kinds of expenses can you deduct? The key phrase that the IRS uses is anything that is “regular and necessary” for the business. A good guideline is right on the Schedule C form. Here’s a link to it right here: Schedule C. Advertising, legal and professional fees, auto expenses, insurance, rent, repairs and maintenance, supplies, and office expenses. Meals and entertainment are deducted at 50% of what you spend (since the idea is that you’d have to eat anyway.)

If this is your first time filing taxes for your small business. I recommend getting a professional to help you. Even if you have a knack for the paperwork, it really helps to have someone else go over the possibilities of what you can deduct and make sure that the big things like depreciation (if you have that) are handled correctly. If you get started on the right track, it’s easier to stay that way.

Timing is everything, isn’t it? The new St Louis County property tax increases just got posted on the county website yesterday. My taxes went up $235. Although I hate having to pay more, it’s still less than my 2008 tax rate. So I guess I shouldn’t complain too much.

But I’m in the Parkway school district, our school district taxes only went up 4.61%. People living in the Pattonville district, which happens to be a few streets over from my house, had an 11.5% increase. Other districts with double digit percentage increases are Brentwood, Maplewood-Richmond Heights, University City and Webster Groves.

If you want to check out your new tax bill, click on this link. It will take you to the real estate tax information for St Louis County.

http://revenue.stlouisco.com/ias/

You can find your property by typing in your name or your address. That will take you to the page that tells about your property, it has assessment values, legal description, and things like that. In the light blue column on the left hand side, there is a link that says “Tax Amounts Due.” It’s close to the bottom of the page. Click on that. Scroll down towards the bottom of the page and it will show you your 2010 tax amount.

It’s really not that hard to navigate. You just have to remember that the “finder” portion of the page is always at the very bottom. You need to be in the top half of the screen and scroll to find some of the things I’m talking about. It’s not always intuitive. A wrong click can make you start over.

The St Louis Post Dispatch did a good article on the subject in today’s paper. Here’s a link to the full story. Post Dispatch article

photo by S.E.B.

But people seem to want me to. I often get calls from people telling me they know someone is cheating on their taxes and they want me to report them. First and foremost, I am not the IRS. If you truly believe that someone is cheating on their taxes and you really want to report it, you have to report it directly to the IRS.

I think the main reason that people call me is they’ve called the IRS first and “nothing happened.” That’s quite possible, and here’s why. For one thing, if you really are reporting tax fraud, you need to fill out form 3949 and mail it to: Internal Revenue Service, Fresno, CA 93888.

Here’s a link to get the form on the IRS website.

http://www.irs.gov/pub/irs-pdf/f3949a.pdf

A phone call won’t do the trick. The IRS wants its paperwork. It has to be the right paperwork and it has to go to the right place.

Second, when completing the form, only answer the questions asked–see the second page of the form for a more detailed explanation of what they’re looking for. Don’t send the IRS anything not specifically asked for. If the IRS is going to build a successful case, they will have to do the work themselves. They have access to an amazing amount of information plus they have the power of subpoena. If they want your evidence, they will ask you for it (but don’t hold your breath.)

Unless you are a crucial witness to the case, you will hear nothing about the audit from the IRS. They won’t even tell you if they perform one. You cannot call them to learn about the audit because the IRS will not be able to tell you anything, it would be a violation of privacy laws. Once you’ve mailed in that form– you’re done. There will never be a phone call thanking you for your assistance. You won’t see the police come and cart the person away. If you’re seeking revenge, you’ll never know if you got it or not.

Here’s another tip: look closely at your motives for reporting the fraud. Are you genuinely trying to report a real tax crime or are you mad at your ex-husband for not paying the child support while buying his new girlfriend a diamond ring? The IRS really does not want to be involved in personal domestic squabbles.

If you are reporting a former spouse, look long and hard at what you’re doing. It’s quite possible that an audit could come back at you. Let’s say you’ve only been divorced for a few months and the IRS performs an audit. If they find that your ex-husband was under-reporting income, they are likely to investigate prior years. If they find that he owes taxes for years that you were married to him, you could be held liable for paying those taxes. Stop and think before you act.

One final thing, if your complaint is that someone claimed your children on his or her return and shouldn’t have, don’t file a 3949 form. Just prepare your return correctly, listing your children as dependents, and mail it in. The IRS will take it from there.

Hi. Thanks for visiting us at the Westport Plaza Halloween Parade. Please click on the link below to find the picture of your child. The number on your Treasure Map should coincide with your child’s picture, but I did get a little off so you’ll probably need to add about 5 to get to the right picture. You’ll see the numbers as you scroll the mouse over the photos. (You probably don’t even need the numbers, you’ll see your child anyway.)

Hi. Thanks for visiting us at the Westport Plaza Halloween Parade. Please click on the link below to find the picture of your child. The number on your Treasure Map should coincide with your child’s picture, but I did get a little off so you’ll probably need to add about 5 to get to the right picture. You’ll see the numbers as you scroll the mouse over the photos. (You probably don’t even need the numbers, you’ll see your child anyway.)

Thank you so much for letting us celebrate this event with your family. We probably had as much fun as the kids did.

Pirate Bill and Picture taker Jan

And in case you haven’t already clicked ahead to find your pictures, here’s our brazenly commercial plug: We hope that you’ll consider Roberg Tax Solutions in the future if you need tax assistance. If you’re a do it yourself type, do check back at this site for tips and tricks for preparing your own return. Or, if you’d like, you can sign up for our email newsletter. It comes out once a month. (Of course, we never sell or give out your email address and once you unsubscribe–we don’t bug you again!) You can check out some of our previous newsletters by checking out the archive:

Here’s the e-mail sign up.

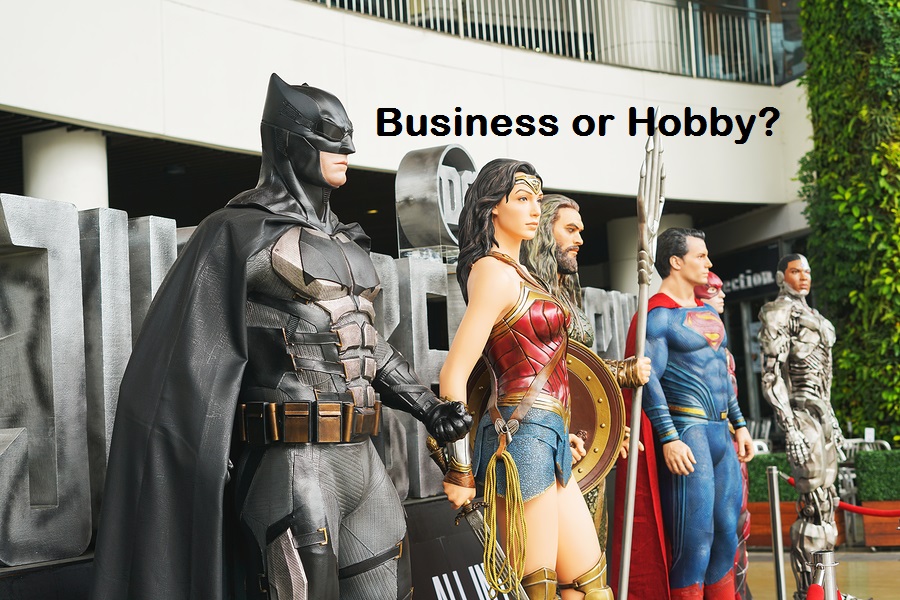

Photo of life size action figures at a gaming event in Thailand.

Updated December 6, 2018

Batman stopped by my office the other day. He usually doesn’t visit me in his Bat costume, but he had just done a charity fundraiser as Batman and had promised the ladies in my office to visit us in costume. (I’d just like to point out that not all of my friends and clients are super heroes. I do know plenty of normal people.)

I once did a post about a fellow who made a business out of appearing as Superman. On a good day, Superman can take in some decent money. After Batman’s successful fundraiser, he kind of wondered aloud about following in Superman’s footsteps and making occasional appearances for pay also. While I recently made the case for Superman being a legitimate business, Batman’s income I believe would be a hobby.

How do you tell if something is a business or a hobby? Sometimes it’s kind of hard to tell. Everybody recognizes that if you open up an Ace Hardware store selling tools and duct tape you’ve got yourself a real business. But what if you make purses and wallets out of duct tape and sell them at craft fairs? Where does that fit in? What if you breed your champion Cocker Spaniel and sell the puppies? Dog breeding is a real business, but how many litters makes you a breeder? It’s not all black and white. Here are some guidelines to help you.

First, I want to point out the most important key ingredient that the IRS uses to determine if you are a real business: a 1099MISC showing an amount under “non-employee compensation.” There are numerous guidelines as to what constitutes a business versus a hobby and this one is never mentioned. Yet it’s the most important factor as far as the IRS is concerned! If you receive a 1099MISC, the IRS counts that as self-employment and they will tax you not just income tax, but an additional 15% self employment tax. As a professional preparer, if I see one of those, even if I truly believe that your business should be classified as a hobby, I’m preparing a Schedule C showing you as a business. That’s how the IRS is treating that income.

What’s the difference in how your income is classified and why is it important? Business income is taxed at your regular income tax rate plus the self employment tax rate. Let’s say your regular tax rate is 22%, then your business income is taxed at 37% (22% + 15% = 40%.) The advantage of being treated as a business is that you can write off your direct business expenses against the income and you can even have a loss that will offset your other income.

Hobby income is taxed at your regular tax rate, there is no self employment tax so you pay less tax on hobby income. The big disadvantage to claiming income as hobby income is that under the new tax law for 2018, you can’t deduct your Hobby expenses. (Although to be fair, it wasn’t a very good deduction before 2018 anyway.)

You cannot switch your business back and forth from hobby to business depending upon whether or not you have a profit or loss. It’s okay to grow your hobby into a business. It’s even okay to downgrade your business into a hobby. But flip flopping for the sake of lowering your taxes is just going to land you in trouble with the IRS. You need to put a little thought into it before you start claiming business losses.

If you’re not receiving 1099 MISC forms, what other tests can you use to prove your business is real and not a hobby? One is the three year test–if you’ve shown a profit in three out of the past five years, then you’re considered a business. This is a good rule, but it’s not completely hard and fast. There are court cases proving businesses to be valid even though they’ve shown losses for more than three years. Even though its a good rule of thumb, I don’t like to see people get too hung up on it, there are other tests.

Is the business carried out with the intention to make a profit? Does the taxpayer (or the taxpayer’s advisors) have the knowledge to make the business a success? Does the taxpayer spend enough time on the business to indicate a profit motive? Has the taxpayer made a profit on similar activities in the past? The answers to these questions is why I put Superman in the business category and not the hobby category. Superman had previous paid experience as a costumed character and model, and he also had a website devoted to his business and posted blogs about how to be a superhero. He clearly devotes a great deal of time to his business. Batman,on the other hand, wouldn’t really pass these tests, that’s why I consider his income to be hobby income.

Me with my Batman friend back in 2010

One final point. Batman takes offense at Batman being labeled as a hobby. “Batman isn’t a hobby, it’s a calling.” Like I said in the beginning, some of my friends are normal.

Charlee Chartrand as Superman from the Post Dispatch article, see link for full story.

What do you do for a living? Are you in advertising, construction, real estate? When you tell people what your job is do they seem to have a grasp of what that means? Some people’s jobs aren’t so easily defined, like Superman for example.

Actually, his name is Charlee Chartrand and he dresses as Superman for his job. This is not your every day occupation. Now I don’t know Mr. Chartrand and I don’t do his taxes, if I did, my confidentiality rules wouldn’t allow me to talk about him. I read about him in Sunday’s Post Dispatch. I did contact him and ask for his permission to use him as an example though.

The main part of Mr. Chartrand’s job is that he dresses as Superman, hangs around at Cardinals games and collects tips for posing in pictures with fans and tourists. He’s also been performing at birthday parties. If you think there’s no money in this, think again, he can earn as much as $400 in tips in a day. And that’s why he’s going to need to figure out his deductions before he files his tax return.

So what can Superman deduct? Let’s hit the obvious thing first: the costume–all of it. Cleaning, repairing, replacing, clearly this is one clothing expense that will count as a business expense. I would also include his undergarmets. You can’t dress as Superman and wear any old boxer shorts.

The hair: most of the time hair cuts and styling products, etc are not considered legitimate expenses for business, even if you are a professional actor or television personality. In Superman’s case here, I would claim his hair expenses. He has to dye his hair black to be Superman, and he uses four different products to get just the right effect–including the “S” shaped curl on his forehead. I think that goes far beyond what would be normal for Mr. Chartrand during his off duty hours.

I can’t tell from the photo if Superman is wearing make-up or not. He doesn’t look like it, but if he was, I’d allow it. (He might need to darken his eyebrows to match his hair.) A note about make-up: generally, make up is frowned upon by the IRS as a business expense. A clown wearing clown make-up would qualify for a deduction, but most women in any business would not. I once helped a dancer with her return and as we went through her expenses she claimed “a gallon of eyelash glue.” Now, I thought that was an excessive amount even for a professional dancer. “Not for eyelashes,” she said, “It’s to keep my costume on!” Evidently, during a dress rehearsal she had had a “wardrobe malfunction”. In order to keep herself looking decent, she glued her costume on to make sure she stayed covered. That clearly fit the category of “necessary” and I put it in. (Even the meanest IRS agent couldn’t argue that one.)

Let’s get back to Superman, He can probably claim either a home office deduction or rent for his work space. And, since he travels from his home office to his gigs, he can deduct his mileage as well. These are expenses that are pretty normal for many small businesses. It’s important to remember that even unusual businesses have normal types of expenses. Another normal type of expense for Superman might be advertising, if he has flyers or cards that he distributes to get new business.

Here’s another expense that I would use for Superman that might seem out of the ordinary: comic books—Mr Chartrand uses comic books to compare against his costume and maintain the authenticity of his look. I’d count it as a valid business expense.

Also, Mr. Chartrand has a goal of moving to Los Angeles. Making a permanent move to Los Angeles would count as a moving expense, as opposed to a business expense. But, if Mr. Chartrand makes a trip to Los Angeles, to test the market so to speak, he could probably write off most of that stay as a business deduction. This would give him a chance to test out the market and give himself an out to come home if he found Los Angeles wasn’t the place for him.

When claiming business deductions, the key phrase the IRS uses is “ordinary and necessary”.

To be deductible, a business expense must be both ordinary and necessary. An ordinary expense is one that is common and accepted in your field of business. A necessary expense is one that is helpful and appropriate for your business. An expense does not have to be indispensable to be considered necessary.

When you’ve got a one-of-a- kind type of career, it’s not always easy to figure out what ordinary means. Hopefully, Superman’s example can give you some ideas about what’s ordinary and necessary for your business.

To read more about Charlee Chartrand, aka Superman, this link will take you to the St. Louis Post-Dispatch article about him:

A real deer in headlights, not my husband.

I was having dinner with my husband and was telling him that we needed to think about doing a Roth IRA conversion this year. The more detail I went into, the further his eyes glazed over. Finally, he waved his hand over his head and said, “You do the calculations and let me know if we should or not.” He gets that way when I go into “tax speak.” He’s not stupid either, he understands money, he has an MBA, but taxes tend to give him that deer in the headlights look. I’m guessing he’s not alone. Here’s my attempt at making it easy.

A regular IRA is money that you get a tax deduction for when you put the money in, but you pay taxes on it when you take the money out. If you take the money out before you’re 59 1/2, you also pay a 10% penalty on top of the tax you pay for taking it out.

A Roth IRA doesn’t give you any tax deduction when you put the money in, but when you take it out there is no tax on the withdrawl. The penalty, if you take it out early, is only on the earnings, not the main amount of money. It’s usually very small.

The whole issue of Roth vs regular is Pay Now or Pay Later. Normally I’m a “pay later” kind of person, but I like the benefits of the Roth so much that they often outweigh the disadvantage of Pay Now.

So what’s a Roth conversion? That’s when you have money that you put into a regular IRA and move it into a Roth IRA. When you do that, you will have to pay tax on the IRA money, but you won’t have to pay the penalty.

Why would anyone want to do that? It’s back to pay now versus pay later. It looks like tax rates will go up in the future. Roth IRA money would be tax-free income during retirement and we all like tax free income!

Why is it a big deal now? Normally, you can only convert to a Roth IRA if your income is less than $100,000 — that’s including the money being moved into a Roth IRA because that also counts as income. For this year only, 2010, there is no income limit. Anybody can play.

So what’s the catch? If you do a conversion, you have to pay the tax. You have two choices: 1. You pay all of the tax on the conversion with your 2010 tax return, or 2. You split the tax you pay into two equal installments with your 2011 and 2012 taxes.

Once again, normally I’m a pay later person, but right now Congress hasn’t extended the Bush tax cuts yet. Until we hear otherwise, tax rates are scheduled to go up for 2011. I’d make my decision based upon paying it all in 2010. If things change, then you’ve got options, otherwise, go for pay now.

Do I have to convert all of the money in my IRA to a Roth? No. Only as much as you want/can afford to.

Do you think I should do it? That depends. The younger you are, the more inclined I am to say yes. If you’ve ever put money into an IRA that you didn’t get a deduction for, I’m more inclined to say yes. How are you going to pay the additional tax? If you’re going to take it out of the IRA money you withdraw, then I’m definitely leaning against that. If’ you’ve got it in savings, or have withheld extra and are just giving up a big refund, then you’re good.

Bottom line is: as much as I like Roth IRAs and this is a once in a lifetime opportunity, it also involves paying more taxes. If you have the cash and can afford to do it, I say go for it. If you’re cash strapped already, it’s not such a good choice.

I often hear the question, “When should a person do his/her own tax return?” Now nobody ever asks me that directly, as a professional preparer you’d think I’d say, “Always!” And yeah, that’s pretty much my general answer. But let’s face it, right now money is tight for everyone and if you can keep more of your money in your pocket by doing something yourself, maybe you should.

I often hear the question, “When should a person do his/her own tax return?” Now nobody ever asks me that directly, as a professional preparer you’d think I’d say, “Always!” And yeah, that’s pretty much my general answer. But let’s face it, right now money is tight for everyone and if you can keep more of your money in your pocket by doing something yourself, maybe you should.

Here’s a clue: How long does it take for someone to do your taxes for you? I was reading in the paper today about a guy who whipped out tax returns for clients at an average rate of 15 minutes per return. If your preparer can finish your return in 15 minutes, that’s not tax preparation–that’s data entry. If you’ve just got a simple data entry type return, then you can probably do it yourself for free online.

Here’s an example: Peggy is a single person living in Missouri making $35,000 a year (roughly the median income for a single person her age.) Working a regular wage earning job, she’ll have $2,170 taken out for social security and $508 taken out for medicare taxes. Her federal income tax for the year will be $3,434 and her state income tax will be $1,225. So, for the year, she’s paying $7,337 in income related taxes alone. That’s almost 21% of her income.

If you’re going to spend 20% or more of your annual income on something, don’t you think it deserves more than 15 minutes of attention? If I were doing Peggy’s taxes, we’d be talking about her plans–does she want to buy a house? get married? go back to school? save for retirement? etc. We’d also talk about her job, what kind of benefits are available, is she taking advantage of those programs, etc. We’d also be talking about any ways that might be available for Peggy to reduce paying 21% of her income towards taxes.

It’s quite possible that there’s nothing there for Peggy. There are no possible deductions for her, she doesn’t care about retirement, she just wants her taxes to be filed and be done with it. Mr. 15 Minutes is good enough for her. In that case, why pay him when she can do it herself? Peggy would be a prime candidate for doing her own taxes.

Twenty percent of your income deserves more than 15 minutes of thought. If you’re going to a 15 Minute Man, that’s all you’ll get and you really would be better off doing it yourself.